# Vehicle Financing

**Transform how you acquire equipment on your farm**

Vehicle Financing in UsedPlus replaces the vanilla "buy or lease" dichotomy with a realistic financing system that mirrors real-world farm equipment loans. Instead of paying full price upfront or being locked into a lease, you can finance any vehicle or implement with flexible terms ranging from 1 to 15 years.

---

## Table of Contents

1. [Overview](#overview)

2. [How to Finance a Vehicle](#how-to-finance-a-vehicle)

3. [Loan Terms](#loan-terms)

4. [Down Payment](#down-payment)

5. [Interest Rates](#interest-rates)

6. [Monthly Payments](#monthly-payments)

7. [Early Payoff](#early-payoff)

8. [Ownership & Flexibility](#ownership--flexibility)

9. [Credit Score Impact](#credit-score-impact)

10. [Finance vs Lease Comparison](#finance-vs-lease-comparison)

11. [Tips & Strategies](#tips--strategies)

---

## Overview

### What is Vehicle Financing?

**Vehicle Financing** allows you to purchase equipment by paying a down payment (0-50% of the price) and spreading the remaining cost over monthly installments. Unlike leasing, **you own the vehicle immediately** and can modify, sell, or trade it at any time.

### Why Finance Instead of Buying Outright?

- **Preserve Cash Flow** - Keep capital available for seeds, fertilizer, and operations

- **Scale Faster** - Acquire equipment sooner rather than waiting to save full price

- **Build Credit** - On-time payments improve your credit score, unlocking better terms in the future

- **Flexibility** - Pay extra when cash is good, or make minimum payments during tight months

### Key Differences from Vanilla

| Aspect | Vanilla FS25 | UsedPlus Financing |

|--------|--------------|-------------------|

| Payment Options | Buy outright or lease | Buy, finance, or lease |

| Ownership | Immediate (buy) or deferred (lease) | **Immediate ownership** |

| Terms | Fixed lease duration | **1-15 year flexible terms** |

| Credit Impact | None | **Builds or damages credit score** |

| Early Exit | Lease penalties | **Payoff anytime, save interest** |

| Sell Anytime | Yes (buy) or No (lease) | **Yes - you own it** |

---

## How to Finance a Vehicle

### Step-by-Step: Financing from the Shop

1. **Open the Shop** and browse to any vehicle or implement

2. **Click the vehicle** to view details

3. **Click "Finance"** button (replaces vanilla "Buy" if override enabled, or separate button)

4. **Unified Purchase Dialog opens** with three tabs:

- Cash (pay full price)

- **Finance** (what we're here for!)

- Lease (balloon payment option)

5. **Configure Your Finance Deal:**

- **Down Payment**: Slider from 0% to 50%

- **Loan Term**: Dropdown from 1 to 15 years (credit-gated)

- **Trade-In** (optional): Apply old equipment value toward purchase

6. **Review the Summary:**

- Monthly payment amount

- Total interest paid over life of loan

- Total cost (principal + interest)

- Your credit score and interest rate

7. **Click "Confirm"** to complete the purchase

8. **Vehicle is yours immediately** - drive it off the lot!

Finance tab showing loan configuration with down payment, term selection, and monthly payment calculation

Loan approval confirmation with deal summary and next steps

### Hotkeys

- **U** - Open Used Search dialog (from shop)

- **Esc** → Finance Manager - Open Finance Manager (anywhere)

---

##  Loan Terms

### Available Term Lengths

Vehicle financing offers terms from **1 year to 15 years**, but longer terms are **credit-gated** to ensure you have the financial stability to handle extended debt.

| Term Range | Credit Requirement | Monthly Payment | Total Interest | Use Case |

|------------|-------------------|----------------|----------------|----------|

| **1-5 years** | Any credit score | High | Low | Short-term needs, good cash flow |

| **6-10 years** | Fair (650+) | Moderate | Moderate | Balanced approach |

| **11-15 years** | Good (700+) | Low | High | Maximize cash flow, long-term assets |

### Credit Tier Requirements & Benefits

Your credit score doesn't just affect your interest rate - it also **gates what financing options are available** to you:

| Credit Rating | Score Range | Max Term | Min Down Payment | Interest Modifier |

|---------------|-------------|----------|------------------|------------------|

| **Excellent** | 750-850 | 15 years | **0%** (no down payment required!) | -1.5% |

| **Good** | 700-749 | **15 years** | 5% | -0.5% |

| **Fair** | 650-699 | **10 years** | 10% | +0.5% |

| **Poor** | 600-649 | 5 years | 20% | +1.5% |

| **Very Poor** | <600 | 5 years | **25%** (must have skin in game) | +3.0% |

**Key Insights:**

- **Term gating** prevents over-leveraging: New farmers can't take on 15-year debt they can't afford

- **Down payment minimums** ensure you have capital investment: Banks want to see you have "skin in the game"

- **Excellent credit unlocks 0% down**: This is the "gold standard" - banks trust you completely

**Important:** Land financing can extend up to **20 years** with Good credit (see [Land Financing](Land-Financing.md) for details).

### How Term Length Affects Your Deal

**Example: $100,000 Tractor, 10% down ($90,000 financed), 8.5% APR (Fair credit)**

| Term | Monthly Payment | Total Interest | Total Paid | Monthly Cash Flow Impact |

|------|----------------|----------------|------------|--------------------------|

| 3 years | $2,843 | $12,348 | $112,348 | High impact, quick payoff |

| 5 years | $1,844 | $20,640 | $120,640 | Moderate impact |

| 10 years | $1,115 | $43,800 | $133,800 | Low impact, expensive |

| 15 years | $887 | $69,660 | $159,660 | Very low impact, very expensive |

**Strategy Tip:** Shorter terms save money but require higher monthly payments. Choose based on your farm's cash flow, not just what you qualify for.

---

## Down Payment

### Down Payment Range: 0% to 50% (Credit-Gated)

You can finance up to **100% of the purchase price** (0% down with Excellent credit) or reduce your loan with a down payment of up to **50%**.

**Important:** Your **minimum down payment** is determined by your credit score:

- Excellent (750+): **0% minimum** - can finance 100% if desired

- Good (700-749): **5% minimum**

- Fair (650-699): **10% minimum**

- Poor (600-649): **20% minimum**

- Very Poor (<600): **25% minimum** - must show commitment

### How Down Payment Affects Your Deal

**Example: $100,000 Tractor, 5 year term, 8.5% APR (Fair credit, average down payment)**

| Down Payment | Amount Financed | Monthly Payment | Total Interest | Total Cost |

|--------------|----------------|----------------|----------------|------------|

| **0% ($0)** | $100,000 | $2,052 | $23,120 | $123,120 |

| **10% ($10,000)** | $90,000 | $1,847 | $20,820 | $120,820 |

| **25% ($25,000)** | $75,000 | $1,539 | $17,340 | $117,340 |

| **50% ($50,000)** | $50,000 | $1,026 | $11,560 | $111,560 |

### Down Payment Strategy

| Situation | Recommended Down Payment | Reason |

|-----------|-------------------------|--------|

| **Starting Out** | 0-10% | Preserve cash for operations |

| **Stable Income** | 20-30% | Balance cash flow and interest savings |

| **Strong Cash Position** | 40-50% | Minimize interest, build equity fast |

| **Credit Building** | 10-20% | Manageable debt-to-asset ratio |

**Pro Tip:** If you have excellent credit and low monthly obligations, financing at 0% down lets you invest that capital elsewhere (land, livestock, supplies) while paying minimal interest.

---

##

Loan Terms

### Available Term Lengths

Vehicle financing offers terms from **1 year to 15 years**, but longer terms are **credit-gated** to ensure you have the financial stability to handle extended debt.

| Term Range | Credit Requirement | Monthly Payment | Total Interest | Use Case |

|------------|-------------------|----------------|----------------|----------|

| **1-5 years** | Any credit score | High | Low | Short-term needs, good cash flow |

| **6-10 years** | Fair (650+) | Moderate | Moderate | Balanced approach |

| **11-15 years** | Good (700+) | Low | High | Maximize cash flow, long-term assets |

### Credit Tier Requirements & Benefits

Your credit score doesn't just affect your interest rate - it also **gates what financing options are available** to you:

| Credit Rating | Score Range | Max Term | Min Down Payment | Interest Modifier |

|---------------|-------------|----------|------------------|------------------|

| **Excellent** | 750-850 | 15 years | **0%** (no down payment required!) | -1.5% |

| **Good** | 700-749 | **15 years** | 5% | -0.5% |

| **Fair** | 650-699 | **10 years** | 10% | +0.5% |

| **Poor** | 600-649 | 5 years | 20% | +1.5% |

| **Very Poor** | <600 | 5 years | **25%** (must have skin in game) | +3.0% |

**Key Insights:**

- **Term gating** prevents over-leveraging: New farmers can't take on 15-year debt they can't afford

- **Down payment minimums** ensure you have capital investment: Banks want to see you have "skin in the game"

- **Excellent credit unlocks 0% down**: This is the "gold standard" - banks trust you completely

**Important:** Land financing can extend up to **20 years** with Good credit (see [Land Financing](Land-Financing.md) for details).

### How Term Length Affects Your Deal

**Example: $100,000 Tractor, 10% down ($90,000 financed), 8.5% APR (Fair credit)**

| Term | Monthly Payment | Total Interest | Total Paid | Monthly Cash Flow Impact |

|------|----------------|----------------|------------|--------------------------|

| 3 years | $2,843 | $12,348 | $112,348 | High impact, quick payoff |

| 5 years | $1,844 | $20,640 | $120,640 | Moderate impact |

| 10 years | $1,115 | $43,800 | $133,800 | Low impact, expensive |

| 15 years | $887 | $69,660 | $159,660 | Very low impact, very expensive |

**Strategy Tip:** Shorter terms save money but require higher monthly payments. Choose based on your farm's cash flow, not just what you qualify for.

---

## Down Payment

### Down Payment Range: 0% to 50% (Credit-Gated)

You can finance up to **100% of the purchase price** (0% down with Excellent credit) or reduce your loan with a down payment of up to **50%**.

**Important:** Your **minimum down payment** is determined by your credit score:

- Excellent (750+): **0% minimum** - can finance 100% if desired

- Good (700-749): **5% minimum**

- Fair (650-699): **10% minimum**

- Poor (600-649): **20% minimum**

- Very Poor (<600): **25% minimum** - must show commitment

### How Down Payment Affects Your Deal

**Example: $100,000 Tractor, 5 year term, 8.5% APR (Fair credit, average down payment)**

| Down Payment | Amount Financed | Monthly Payment | Total Interest | Total Cost |

|--------------|----------------|----------------|----------------|------------|

| **0% ($0)** | $100,000 | $2,052 | $23,120 | $123,120 |

| **10% ($10,000)** | $90,000 | $1,847 | $20,820 | $120,820 |

| **25% ($25,000)** | $75,000 | $1,539 | $17,340 | $117,340 |

| **50% ($50,000)** | $50,000 | $1,026 | $11,560 | $111,560 |

### Down Payment Strategy

| Situation | Recommended Down Payment | Reason |

|-----------|-------------------------|--------|

| **Starting Out** | 0-10% | Preserve cash for operations |

| **Stable Income** | 20-30% | Balance cash flow and interest savings |

| **Strong Cash Position** | 40-50% | Minimize interest, build equity fast |

| **Credit Building** | 10-20% | Manageable debt-to-asset ratio |

**Pro Tip:** If you have excellent credit and low monthly obligations, financing at 0% down lets you invest that capital elsewhere (land, livestock, supplies) while paying minimal interest.

---

##  Interest Rates

### Base Interest Rates

UsedPlus uses **realistic interest rates** that vary by loan type and credit score. Vehicle financing starts with a **base rate** that's higher than land loans (vehicles depreciate, land appreciates).

| Loan Type | Base Rate | Reason |

|-----------|-----------|--------|

| **Vehicle Financing** | 8.0% | Depreciating asset, higher risk |

| **Land Financing** | 7.0% | Appreciating asset, lower risk |

| **General Loans** | 8.0% | Unsecured, same as vehicles |

**Note:** Base rates can be adjusted in mod settings. These are the default values.

### Credit Score Modifiers

Your credit score **directly affects your interest rate** through a modifier applied to the base rate:

| Credit Rating | Score Range | Interest Modifier | Effective Rate (Vehicle) |

|---------------|-------------|------------------|--------------------------|

| **Excellent** | 750-850 | **-1.5%** | 6.5% |

| **Good** | 700-749 | **-0.5%** | 7.5% |

| **Fair** | 650-699 | **+0.5%** | 8.5% |

| **Poor** | 600-649 | **+1.5%** | 9.5% |

| **Very Poor** | <600 | **+3.0%** | 11.0% |

**Note:** Additional adjustments apply based on term length (0% to +1.5%) and down payment (-1.0% to +1.0%), so your actual rate may vary from these base effective rates.

### Real-World Impact

**Example: $100,000 Tractor, 0% down, 10 year term (base rates, no term/down payment adjustments)**

| Credit Score | Interest Rate | Monthly Payment | Total Interest | Difference vs Excellent |

|--------------|---------------|----------------|----------------|-------------------------|

| **800 (Excellent)** | 6.5% | $1,136 | $36,320 | - |

| **720 (Good)** | 7.5% | $1,187 | $42,440 | +$6,120 |

| **670 (Fair)** | 8.5% | $1,239 | $48,680 | +$12,360 |

| **620 (Poor)** | 9.5% | $1,292 | $55,040 | +$18,720 |

| **550 (Very Poor)** | 11.0% | $1,379 | $65,480 | +$29,160 |

**Key Insight:** A Very Poor credit score costs you **$29,160 more in interest** over 10 years compared to Excellent credit. Building credit is worth real money!

**Note:** Actual rates may be slightly different due to term length and down payment adjustments. Use the in-game finance dialog for exact calculations.

### How Interest is Calculated

UsedPlus uses **amortized loan** calculations, the same method used by real banks:

```

Formula:

M = P × [r(1 + r)^n] / [(1 + r)^n - 1]

Where:

M = Monthly payment

P = Principal (amount financed)

r = Monthly interest rate (annual rate ÷ 12)

n = Number of months

```

**What This Means for You:**

- Early payments are mostly interest, later payments are mostly principal

- Paying extra early in the loan saves the most interest

- Your monthly payment stays the same, but the split between interest and principal changes over time

---

## Monthly Payments

### When Payments Are Due

Payments are **automatically deducted** from your farm account on the **1st in-game day of each month** at approximately **6:00 AM**.

**Important:** If you don't have sufficient funds, you'll **miss the payment**, which damages your credit score and starts the seizure countdown.

### Payment Breakdown: Where Your Money Goes

Every monthly payment is split between **interest** (what the bank charges you) and **principal** (what reduces your loan balance).

**Example: $100,000 loan at 8.5% APR (Fair credit), 5 year term**

| Month | Monthly Payment | Interest Paid | Principal Paid | Remaining Balance |

|-------|----------------|---------------|----------------|-------------------|

| 1 | $2,052 | $708 | $1,344 | $98,656 |

| 6 | $2,052 | $675 | $1,377 | $92,240 |

| 12 | $2,052 | $625 | $1,427 | $83,160 |

| 24 | $2,052 | $498 | $1,554 | $61,360 |

| 36 | $2,052 | $356 | $1,696 | $38,040 |

| 48 | $2,052 | $201 | $1,851 | $13,240 |

| 60 | $2,052 | $14 | $2,038 | $0 |

**Notice:** In month 1, only $1,344 goes toward your loan balance. By month 60, almost the entire payment ($2,038) reduces the balance. This is why **paying extra early** saves the most money.

### Amortization Schedule

You can view your **full amortization schedule** in the Finance Manager:

1. Open Finance Manager (press **Esc** → Finance Manager)

2. Click any finance deal

3. Click "View Details"

4. See month-by-month breakdown

Interest Rates

### Base Interest Rates

UsedPlus uses **realistic interest rates** that vary by loan type and credit score. Vehicle financing starts with a **base rate** that's higher than land loans (vehicles depreciate, land appreciates).

| Loan Type | Base Rate | Reason |

|-----------|-----------|--------|

| **Vehicle Financing** | 8.0% | Depreciating asset, higher risk |

| **Land Financing** | 7.0% | Appreciating asset, lower risk |

| **General Loans** | 8.0% | Unsecured, same as vehicles |

**Note:** Base rates can be adjusted in mod settings. These are the default values.

### Credit Score Modifiers

Your credit score **directly affects your interest rate** through a modifier applied to the base rate:

| Credit Rating | Score Range | Interest Modifier | Effective Rate (Vehicle) |

|---------------|-------------|------------------|--------------------------|

| **Excellent** | 750-850 | **-1.5%** | 6.5% |

| **Good** | 700-749 | **-0.5%** | 7.5% |

| **Fair** | 650-699 | **+0.5%** | 8.5% |

| **Poor** | 600-649 | **+1.5%** | 9.5% |

| **Very Poor** | <600 | **+3.0%** | 11.0% |

**Note:** Additional adjustments apply based on term length (0% to +1.5%) and down payment (-1.0% to +1.0%), so your actual rate may vary from these base effective rates.

### Real-World Impact

**Example: $100,000 Tractor, 0% down, 10 year term (base rates, no term/down payment adjustments)**

| Credit Score | Interest Rate | Monthly Payment | Total Interest | Difference vs Excellent |

|--------------|---------------|----------------|----------------|-------------------------|

| **800 (Excellent)** | 6.5% | $1,136 | $36,320 | - |

| **720 (Good)** | 7.5% | $1,187 | $42,440 | +$6,120 |

| **670 (Fair)** | 8.5% | $1,239 | $48,680 | +$12,360 |

| **620 (Poor)** | 9.5% | $1,292 | $55,040 | +$18,720 |

| **550 (Very Poor)** | 11.0% | $1,379 | $65,480 | +$29,160 |

**Key Insight:** A Very Poor credit score costs you **$29,160 more in interest** over 10 years compared to Excellent credit. Building credit is worth real money!

**Note:** Actual rates may be slightly different due to term length and down payment adjustments. Use the in-game finance dialog for exact calculations.

### How Interest is Calculated

UsedPlus uses **amortized loan** calculations, the same method used by real banks:

```

Formula:

M = P × [r(1 + r)^n] / [(1 + r)^n - 1]

Where:

M = Monthly payment

P = Principal (amount financed)

r = Monthly interest rate (annual rate ÷ 12)

n = Number of months

```

**What This Means for You:**

- Early payments are mostly interest, later payments are mostly principal

- Paying extra early in the loan saves the most interest

- Your monthly payment stays the same, but the split between interest and principal changes over time

---

## Monthly Payments

### When Payments Are Due

Payments are **automatically deducted** from your farm account on the **1st in-game day of each month** at approximately **6:00 AM**.

**Important:** If you don't have sufficient funds, you'll **miss the payment**, which damages your credit score and starts the seizure countdown.

### Payment Breakdown: Where Your Money Goes

Every monthly payment is split between **interest** (what the bank charges you) and **principal** (what reduces your loan balance).

**Example: $100,000 loan at 8.5% APR (Fair credit), 5 year term**

| Month | Monthly Payment | Interest Paid | Principal Paid | Remaining Balance |

|-------|----------------|---------------|----------------|-------------------|

| 1 | $2,052 | $708 | $1,344 | $98,656 |

| 6 | $2,052 | $675 | $1,377 | $92,240 |

| 12 | $2,052 | $625 | $1,427 | $83,160 |

| 24 | $2,052 | $498 | $1,554 | $61,360 |

| 36 | $2,052 | $356 | $1,696 | $38,040 |

| 48 | $2,052 | $201 | $1,851 | $13,240 |

| 60 | $2,052 | $14 | $2,038 | $0 |

**Notice:** In month 1, only $1,344 goes toward your loan balance. By month 60, almost the entire payment ($2,038) reduces the balance. This is why **paying extra early** saves the most money.

### Amortization Schedule

You can view your **full amortization schedule** in the Finance Manager:

1. Open Finance Manager (press **Esc** → Finance Manager)

2. Click any finance deal

3. Click "View Details"

4. See month-by-month breakdown

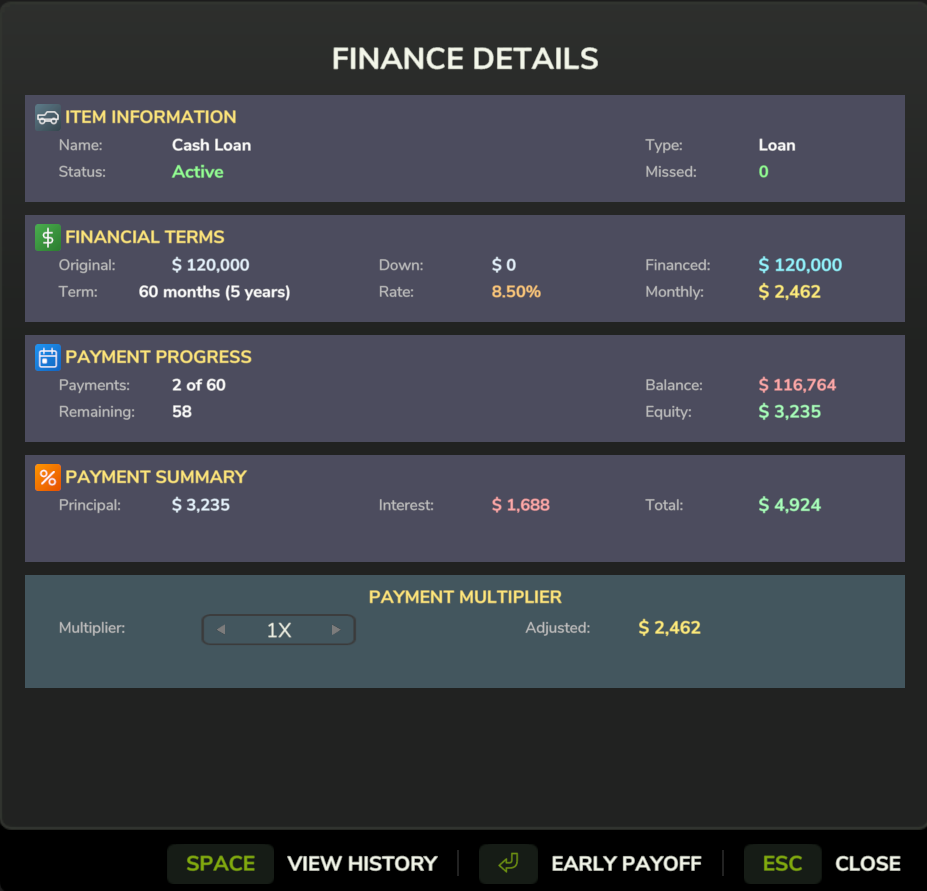

Detailed finance deal view showing loan terms, interest rate, and payment configuration options

Complete amortization schedule showing monthly breakdown of principal vs interest payments

### Payment Configuration Options

UsedPlus allows you to **customize your payment amount** for each loan independently. See [Payment Configuration](#payment-configuration-options) for full details.

Quick summary of options:

| Payment Type | Description | Credit Impact |

|--------------|-------------|---------------|

| **Skip** | No payment, balance grows (negative amortization) | -45 points |

| **Minimum** | Interest-only payment, balance unchanged | 0 points |

| **Standard** | Original amortized payment | +2 points |

| **1.5x Extra** | 50% extra reduces principal faster | +2 points |

| **2x Extra** | Double payment for aggressive payoff | +2 points |

| **Custom** | Set any amount ≥ minimum | Varies |

---

## Early Payoff

### Why Pay Off Early?

Unlike some real-world loans with prepayment penalties, UsedPlus financing has **NO prepayment penalty**. Paying off your loan early:

- **Saves Interest** - Stop paying interest immediately

- **Improves Credit** - +50 credit score bonus

- **Frees Up Debt Capacity** - Lower debt-to-asset ratio unlocks better terms

- **Reduces Monthly Obligations** - More cash flow flexibility

### How to Pay Off Early

1. Open **Finance Manager** (press **Esc** → Finance Manager)

2. Click the finance deal you want to pay off

3. Click **"Pay Early"** button

4. Select **"Pay Off Loan"** option

5. Confirm payment

**Alternative:** Make extra payments over time using the "2x Extra" or "Custom" payment options.

### Interest Savings Example

**Scenario: $100,000 loan at 8.5% APR (Fair credit), 10 year term, paid off after 3 years**

| If You Pay... | Total Interest Paid | Interest Saved | Credit Bonus |

|---------------|-------------------|----------------|--------------|

| **Full 10 years** | $48,680 | - | +5 per payment |

| **Payoff after 3 years** | $14,760 | **$33,920 saved** | **+50 bonus** |

### Strategy: The "Refi After Credit Boost" Play

1. **Year 1-2:** Finance a $50k implement at Fair credit (8.5% APR)

2. **Build Credit:** Make on-time payments, score rises from 650 → 720

3. **Year 3:** Take out a **new loan** at Good credit (7.5% APR) to pay off the old loan

4. **Result:** Lower interest rate on remaining balance, +50 payoff bonus, improved cash flow

---

## Ownership & Flexibility

### Immediate Ownership

When you finance a vehicle, **you own it immediately**. This is fundamentally different from leasing:

| Aspect | Financed Vehicle | Leased Vehicle |

|--------|-----------------|----------------|

| **Ownership** | You own it | Dealership owns it |

| **Sell Anytime** | Yes | No (lease must end) |

| **Trade-In** | Yes | No |

| **Modifications** | Unlimited | None |

| **Damage Penalties** | None | Yes (at lease end) |

| **Balloon Payment** | None | Yes (residual value) |

### What You Can Do with a Financed Vehicle

- **Sell It** - Loan balance must be paid from sale proceeds, you keep the rest

- **Trade It In** - Trade-in value applied toward new purchase, loan paid off

- **Modify It** - Paint, tires, attachments - it's yours

- **Repair It** - Finance repairs if needed (see [FAQ - Repairs](FAQ#how-do-i-repair-a-vehicle))

- **Let It Sit** - No usage requirements, payments continue regardless

### Selling a Financed Vehicle

If you sell a vehicle that still has a finance balance:

1. **Sale proceeds** pay off the loan balance first

2. **Remaining funds** go to you

3. **If sale < balance:** You must pay the difference (negative equity)

**Example:**

- Vehicle sells for $60,000

- Finance balance: $45,000

- You receive: **$15,000** ($60k - $45k)

**Negative Equity Example:**

- Vehicle sells for $30,000

- Finance balance: $45,000

- You must pay: **$15,000** from pocket ($45k - $30k)

**Strategy Tip:** Don't finance 100% of a rapidly depreciating vehicle unless you plan to keep it long-term. You can end up "underwater" (owing more than it's worth).

---

## Credit Score Impact

### How Vehicle Financing Affects Your Credit

Every financial decision you make with vehicle financing impacts your credit score, which in turn affects your future financing options.

### Positive Credit Actions

| Action | Credit Impact | Notes |

|--------|---------------|-------|

| **On-Time Payment** | +2 points | Each month you pay on time |

| **Pay Off Loan Early** | +50 points | One-time bonus |

| **Extra Payment** | +5 points | Same as standard payment |

### Negative Credit Actions

| Action | Credit Impact | Notes |

|--------|---------------|-------|

| **Skip Payment** | -25 points | Balance grows (negative amortization) |

| **Missed Payment** | -25 points | Insufficient funds, not intentional skip |

| **Asset Seized** | -100 points | 3 missed payments triggers seizure |

### Long-Term Credit Building Example

**Scenario: New farmer starts at 650 (Fair) credit**

| Month | Action | Credit Change | New Score |

|-------|--------|---------------|-----------|

| 0 | Start | - | 650 |

| 1-12 | On-time payments (×12) | +60 | 710 |

| 12 | Pay off small loan early | +50 | 760 |

| 13-24 | On-time payments (×12) | +60 | 820 |

**Result:** After 2 years of responsible financing, farmer goes from Fair (650) to Excellent (820), unlocking:

- 15-year vehicle terms (vs 10-year max before)

- 20-year land terms (vs denied before)

- Interest rate drops from 5.0% to 3.0% (saves thousands!)

### Credit Tier Benefits

| Credit Rating | Score | Vehicle Term | Land Term | Interest Modifier | Loan Approval |

|---------------|-------|--------------|-----------|------------------|---------------|

| **Excellent** | 750+ | 15 years | **20 years** | -1.5% | Easy approval |

| **Good** | 700-749 | **15 years** | 20 years | -0.5% | Approved |

| **Fair** | 650-699 | 10 years | 15 years | +0.5% | Approved |

| **Poor** | 600-649 | 5 years | 10 years | +1.5% | Conditional |

| **Very Poor** | <600 | 5 years | **Denied** | +3.0% | High denial risk |

### Debt-to-Asset Ratio

Your **debt-to-asset ratio** is the primary factor in credit scoring (see [Credit Scoring](Credit-Scoring.md) for full details). Vehicle financing affects this ratio:

```

Debt-to-Asset Ratio = Total Debt / Total Assets

Where:

Total Debt = All active loan balances (vehicles, land, cash loans)

Total Assets = Owned vehicles + owned land (at market value)

```

**Strategy:** Keep your ratio below **0.50** (50%) for Good credit, below **0.30** (30%) for Excellent credit.

---

## Finance vs Lease Comparison

### Side-by-Side: Which Should You Choose?

| Factor | Finance | Lease |

|--------|---------|-------|

| **Ownership** | Immediate | At lease end (after balloon) |

| **Down Payment** | 0-50% | 0-20% |

| **Monthly Payment** | Higher | Lower |

| **Can Sell?** | Yes | No |

| **Can Trade-In?** | Yes | No |

| **Damage Penalties** | No | Yes (at end) |

| **Total Cost** | Principal + Interest | Principal + Interest + Balloon |

| **Credit Building** | Yes | Yes |

| **Early Exit** | Anytime, no penalty | Termination fee |

| **Best For** | Long-term ownership | Short-term use, upgrade soon |

### Cost Comparison Example

**Scenario: $100,000 Tractor, 5 year term, 5% APR**

#### Finance Option (25% down)

- Down payment: $25,000

- Amount financed: $75,000

- Monthly payment: $1,416

- Total payments over 5 years: $84,960

- **Total cost: $109,960** (down + payments)

- **You own it free and clear**

#### Lease Option (10% down)

- Down payment: $10,000

- Residual value (balloon): $55,000 (55% of price)

- Amount financed: $35,000 ($100k - $10k down - $55k residual)

- Monthly payment: $662

- Total payments over 5 years: $39,720

- **Balloon payment at end: $55,000**

- **Total cost: $104,720** (down + payments + balloon)

- **You own it if you pay balloon**

**Difference:** Lease costs **$5,240 less** over 5 years, but requires **$55,000 cash at the end** to keep the vehicle.

### When to Finance

Choose **Finance** when:

- You plan to **keep the equipment long-term** (10+ years)

- You want **immediate ownership and flexibility**

- You have **steady cash flow** to handle higher monthly payments

- You want to **build equity** in the equipment

- You plan to **sell or trade-in** within the term

### When to Lease

Choose **Lease** when:

- You plan to **upgrade frequently** (every 3-5 years)

- You want **lower monthly payments** to preserve cash flow

- You have **lumpy income** (harvest sales) and can pay balloon at end

- You want to **test equipment** before committing

- You expect **equipment value to hold** (residual value stays high)

### Strategy: The "Lease-to-Own" Ladder

1. **Year 1:** Lease a $50k implement with $10k down, $400/month

2. **Year 3:** Pay balloon ($27.5k), own outright

3. **Year 3:** Lease a $100k tractor with $20k down, $800/month

4. **Year 6:** Pay balloon ($55k), own outright

5. **Result:** Own $150k in equipment, paid over 6 years, preserved cash flow early on

---

## Tips & Strategies

### Strategy 1: Credit Building First

**Goal:** Start with small loans to build credit, then upgrade to larger equipment with better terms.

1. **Month 1:** Finance a $20k implement at Fair credit (5% APR), 3 year term

2. **Months 1-36:** Make on-time payments (+5 each month = +180 points)

3. **Month 36:** Pay off early (+50 bonus) - Credit rises from 650 → 880 (capped at 850)

4. **Month 37:** Finance a $150k tractor at Excellent credit (3% APR), 15 year term

5. **Result:** Save $30k+ in interest over life of tractor loan

**Key Insight:** Don't rush into massive debt at poor credit terms. Build up first.

---

### Strategy 2: The "Harvest Balloon" Play

**Goal:** Use harvest proceeds to make large principal reductions annually.

1. **Finance** equipment with standard monthly payments

2. **During growing season:** Pay minimum or standard amount

3. **After harvest:** Make **custom payment** of $20k-50k (harvest proceeds)

4. **Result:** Drastically reduce interest paid, own equipment in 2-4 years instead of 10-15

**Example:**

- $100k loan at 8.5% APR (Fair credit), 10 year term

- Standard plan: $1,239/month, $48,680 total interest

- Harvest plan: $1,239/month + $30k/year harvest payment

- **Result:** Paid off in 3 years, only $14,760 interest - **$33,920 saved**

---

### Strategy 3: Zero-Down Expansion

**Goal:** Acquire multiple pieces of equipment quickly with minimal upfront capital.

**Situation:** You have $50k cash. You need a $100k tractor, $50k harvester, and $30k planter.

**Option A: Traditional (Buy Outright)**

- Buy $50k harvester with cash

- Wait years to save for tractor and planter

- **Result:** Limited operation scale, slow growth

**Option B: Finance Everything (0% down at Fair credit, 8.5% APR)**

- Finance $100k tractor: $2,052/month (5 years)

- Finance $50k harvester: $1,026/month (5 years)

- Finance $30k planter: $616/month (5 years)

- **Total monthly: $3,694**

- **Cash remaining: $50k** (for seeds, fuel, operations)

- **Result:** Full operation from day one, high productivity

**Risk:** High monthly obligations. Ensure your farm revenue exceeds $4.5k/month to cover payments + operations.

---

### Strategy 4: The "Trade-Up Ladder"

**Goal:** Continuously upgrade equipment using trade-in value, building equity over time.

1. **Year 1:** Finance $50k tractor (100% financing)

2. **Year 3:** Tractor worth $40k, owe $25k - **$15k equity**

3. **Year 3:** Trade in for $80k tractor:

- Trade-in value: $25k (pays off old loan)

- Finance remaining: $55k ($80k - $25k)

- **New monthly: Lower than before (financing less than original $50k)**

4. **Year 6:** Repeat with $120k tractor

5. **Result:** Always have newer equipment, equity compounds

**Key Insight:** Equity builds fastest in the first half of the loan. Trade-in every 2-3 years to maximize this effect.

---

### Strategy 5: Mixed Term Portfolio

**Goal:** Balance cash flow by mixing short-term and long-term loans.

**Scenario:** You need $200k in equipment.

**Option A: All Long-Term (10 years)**

- Finance $200k at 10 years: $2,122/month

- **Problem:** High total interest ($54,640), slow equity build

**Option B: All Short-Term (3 years)**

- Finance $200k at 3 years: $6,048/month

- **Problem:** Crushing monthly payment

**Option C: Mixed Portfolio (Fair credit, 8.5% APR base)**

- **Tractor ($100k):** 10 year term, $1,239/month - Keep long-term

- **Harvester ($60k):** 5 year term, $1,231/month - Pay off mid-term

- **Planter ($40k):** 3 year term, $1,274/month - Pay off quickly

- **Total Year 1-3:** $3,744/month

- **Total Year 4-5:** $2,470/month (planter paid off)

- **Total Year 6-10:** $1,239/month (harvester paid off)

- **Result:** Manageable payments early, declining obligations over time

**Key Insight:** Finance depreciating assets (harvesters, specialty equipment) short-term. Finance workhorses (tractors) long-term.

---

### Strategy 6: Refinance After Credit Gains

**Goal:** Lower your interest rate by paying off old loans with new loans at better terms.

1. **Start:** $100k loan at Fair credit (8.5% APR), 10 years remaining, $60k balance

2. **After 3 years:** Credit rises to Good (7.5% APR)

3. **Refinance:** Take new $60k loan at 7.5% APR, pay off old loan

4. **Result:**

- Old loan: $1,239/month for 7 more years = $104,076 total

- New loan: $1,193/month for 7 years = $100,212 total

- **Savings: $3,864**

- **Bonus: +50 credit for early payoff**

**When to Refi:** When your credit score improves by 50+ points.

---

### Common Mistakes to Avoid

| Mistake | Why It's Bad | Solution |

|---------|--------------|----------|

| **100% financing on depreciating assets** | Can end up underwater (owe more than it's worth) | Put 10-20% down on harvesters and specialty equipment |

| **Maxing out term length** | Minimizes payment but maximizes interest | Choose shortest term you can comfortably afford |

| **Ignoring credit impact** | Miss payments tanks credit, costs thousands in future interest | Set aside payment buffer, prioritize on-time payments |

| **Buying too much too soon** | High debt-to-asset ratio denies future loans | Start small, build credit, scale up gradually |

| **Not reviewing amortization** | Don't realize how much goes to interest early on | Make extra payments in first 2-3 years to save most |

| **Financing consumables** | Seeds, fuel, etc. don't build equity | Use cash for consumables, finance only capital assets |

---

## Related Topics

- [Credit Scoring](Credit-Scoring.md) - Full credit system explanation

- [Vehicle Leasing](Vehicle-Leasing.md) - Vehicle leasing with balloon payments

- [Land Financing](Land-Financing.md) - Finance farmland purchases

- [Payment Configuration](#payment-configuration-options) - Customize payment amounts

- [Early Payoff](#early-payoff) - Interest savings and credit bonuses

- [Trade-In System](Trade-In-System.md) - Trade old equipment toward new purchases

- [Quick Start Guide](Quick-Start-Guide.md) - Getting started with the Finance Manager

---

*Built with Claude and Samantha - AI-powered farming simulation*