# Vehicle Leasing Guide

A comprehensive guide to leasing vehicles and equipment in FS25_UsedPlus.

---

## Table of Contents

1. [Overview](#overview)

2. [How to Lease](#how-to-lease)

3. [Lease Terms](#lease-terms)

4. [Lower Monthly Payments](#lower-monthly-payments)

5. [Residual Value (Balloon Payment)](#residual-value-balloon-payment)

6. [Buyout Option](#buyout-option)

7. [Return Vehicle](#return-vehicle)

8. [Damage Penalties](#damage-penalties)

9. [Credit Impact](#credit-impact)

10. [Lease vs Finance](#lease-vs-finance)

11. [Tips & Strategies](#tips--strategies)

---

## Overview

### What is Leasing?

**Leasing** is a financing option where you pay to USE a vehicle for a set period, with the option to purchase it at the end of the lease term by paying a final "balloon payment" (the residual value).

Think of it like renting with an option to buy.

### Leasing vs. Financing

| Aspect | Leasing | Financing |

|--------|---------|-----------|

| **Ownership** | Lessor owns, you use | You own immediately |

| **Monthly Payment** | Lower | Higher |

| **Down Payment** | 0-20% | 0-50% |

| **Final Payment** | Residual value (balloon) | None |

| **Can Sell?** | No - leased until buyout | Yes - anytime |

| **Best For** | Short-term use, lower payments | Long-term ownership |

### Key Restrictions

> **WARNING:** Leased vehicles CANNOT be sold or traded in until you complete the buyout. The lessor owns the vehicle - you're just using it.

---

## How to Lease

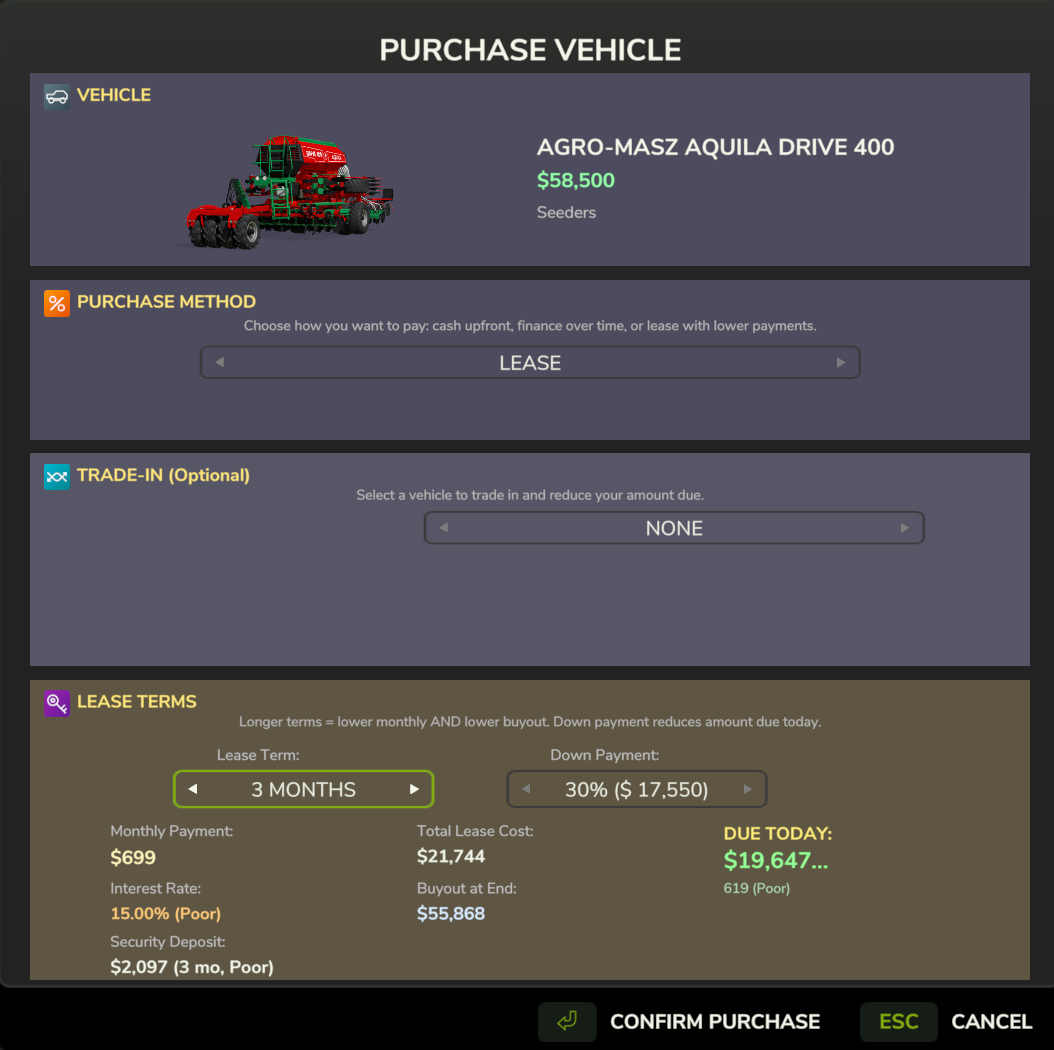

### Step-by-Step from Shop

1. **Open the Vehicle Shop**

- Press the shop icon or visit a dealership

2. **Select Your Vehicle**

- Browse categories and choose equipment

3. **Click "Lease" Button**

- Opens the Unified Purchase Dialog

4. **Configure Your Lease**

- **Down Payment**: 0-20% (lower max than financing's 50%)

- **Term**: 1-5 years (custom lease terms)

- See monthly payment update in real-time

5. **Review Total Cost**

- Monthly payment × term + balloon payment = total cost

- Compare to Cash and Finance options

6. **Confirm Lease**

- Vehicle is added to your fleet

- Marked as "LEASED" in Finance Manager

- Monthly payments begin automatically

Lease configuration showing lower monthly payments with balloon payment at end of term

### Access From Finance Manager

You can also view all active leases in the **Finance Manager** (press **Esc** → Finance Manager):

- Shows monthly payment, remaining term, balloon amount

- Make early payments

- Initiate early termination or buyout

---

##  Lease Terms

UsedPlus offers flexible lease terms from 1 to 5 years.

### Available Terms

| Term | Monthly Payment | Residual Value | Total Interest | Best For |

|------|----------------|----------------|----------------|----------|

| **1 year** | Highest | 65% of price | Lowest | Short-term projects |

| **2 years** | High | 65% of price | Low | Seasonal use |

| **3 years** | Moderate | 55% of price | Moderate | Medium-term needs |

| **4 years** | Lower | 45% of price | Higher | Multi-year operations |

| **5 years** | Lowest | 35% of price | Highest | Long-term use |

### How Terms Affect Residual Value

The **residual value** (balloon payment) decreases with longer lease terms:

```

1-2 years: 65% of original price

3 years: 55% of original price

4 years: 45% of original price

5 years: 35% of original price

```

**Why it matters:** Longer leases mean lower balloon payments at the end, making buyout more affordable.

---

## Lower Monthly Payments

### Why Leasing Has Lower Payments

Leasing payments are lower than financing because **you're only paying for the depreciation during the lease period**, not the full vehicle value.

### Payment Comparison Example

**Scenario:** $100,000 Tractor, 10% down payment, 5% interest rate, 3-year term

#### Finance (Traditional Loan)

```

Principal: $90,000 (100k - 10k down)

Monthly Payment: $2,699

Total Payments: $97,164 (36 months)

Balloon Payment: $0

───────────────────────────────────

TOTAL COST: $107,164 (includes down payment)

YOU OWN IT: After 3 years

```

#### Lease

```

Principal: $90,000 (100k - 10k down)

Residual Value: $55,000 (55% of 100k for 3-year lease)

Effective Loan: $35,000 (90k - 55k)

Monthly Payment: $1,051

Total Payments: $37,836 (36 months)

Balloon Payment: $55,000 (to buy at end)

───────────────────────────────────

TOTAL IF BUYOUT: $102,836 (down + payments + balloon)

YOU OWN IT: After 3 years + balloon payment

```

**Result:**

- Lease monthly payment: $1,051 (61% lower!)

- BUT: Must pay $55k balloon to own it

- Financing total cost: $107,164

- Leasing total cost: $102,836 (saves $4,328 if you buy)

### The Catch

Lower monthly payments come with a tradeoff:

- You don't own the vehicle until you pay the balloon

- You can't sell a leased vehicle

- Early termination has penalties

- Damage at lease end incurs fees

---

## Residual Value (Balloon Payment)

### What is Residual Value?

The **residual value** is the estimated value of the vehicle at the end of the lease term. This is the amount you must pay to purchase (buy out) the leased vehicle.

### Residual Value by Term

| Lease Term | Residual % | Example ($100k Tractor) |

|------------|-----------|-------------------------|

| 1 year | 65% | $65,000 balloon |

| 2 years | 65% | $65,000 balloon |

| 3 years | 55% | $55,000 balloon |

| 4 years | 45% | $45,000 balloon |

| 5 years | 35% | $35,000 balloon |

### How Balloon Payments Work

At the end of your lease term, you have three options:

1. **Pay the balloon and own it** - Pay residual value in full

2. **Return the vehicle** - Walk away (minus damage fees)

3. **Extend/refinance** - Not currently available (future feature)

### Calculating Total Cost with Balloon

```

Total Lease Cost = Down Payment + (Monthly × Term) + Balloon Payment

Example (3-year, $100k tractor, 10% down):

= $10,000 + ($1,051 × 36) + $55,000

= $10,000 + $37,836 + $55,000

= $102,836

```

### Balloon Payment Strategies

**Strategy 1: Pay balloon immediately**

- Own the vehicle outright

- Total cost is down + payments + balloon

**Strategy 2: Finance the balloon**

- Take out a loan for the residual value

- Spreads balloon over additional years

- Converts lease into lease-to-own

**Strategy 3: Return the vehicle**

- Walk away at lease end

- Only paid down + monthly payments

- Good for equipment you only needed temporarily

---

## Buyout Option

### Purchase at Lease End

At the end of your lease term, you can **buy out** the vehicle by paying the residual value (balloon payment).

### Buyout Process

1. **Lease Term Ends**

- You receive notification that lease is complete

- Vehicle remains in your fleet (grace period)

2. **Decide: Buy or Return**

- **Buy:** Pay balloon payment in Finance Manager

- **Return:** Initiate return (damage fees assessed)

3. **After Buyout**

- Vehicle ownership transfers to you

- No more monthly payments

- Can now sell or trade the vehicle

- Full ownership benefits

### Early Buyout

You can buy out a leased vehicle **before** the lease term ends:

#### Early Buyout Formula

```

Early Buyout Cost = Remaining Lease Balance + Residual Value + Early Term Fee

Early Term Fee = 10% of remaining lease balance

```

#### Example: Early Buyout

**Scenario:** 5-year lease on $100k tractor, 2 years remaining

```

Remaining Lease Balance: $25,104 (24 months × $1,046)

Residual Value: $35,000

Early Termination Fee: $2,510 (10% of balance)

───────────────────────────────────────

TOTAL EARLY BUYOUT: $62,614

```

**Compare to:**

- Finishing lease + balloon: $60,104 (cheaper by $2,510)

- Early buyout penalty = 10% fee

**When to buy early:**

- You need to sell the vehicle urgently

- You want to trade it in toward a new purchase

- You found a great deal on a replacement and need cash

---

## Return Vehicle

### End Lease Early

You can return a leased vehicle before the term ends, but it comes with penalties.

### Early Termination Process

1. **Open Finance Manager** (press **Esc** → Finance Manager)

2. **Select Leased Vehicle**

3. **Click "Terminate Lease"**

4. **Damage Assessment**

- Inspector evaluates vehicle condition

- Damage penalties calculated

5. **Pay Termination Fees**

- Early termination fee (10% of remaining balance)

- Damage penalties (if applicable)

6. **Vehicle is Removed**

- Equipment disappears from your fleet

- Returned to lessor

### Early Termination Penalties

| Fee Type | Amount | Example (3-year, $100k tractor, 1 year left) |

|----------|--------|---------------------------------------------|

| **Early Term Fee** | 10% of remaining balance | $1,265 (10% × $12,648) |

| **Damage Fee** | Varies by condition | $0 - $15,000+ |

| **TOTAL PENALTY** | Both fees combined | $1,265 - $16,265+ |

### When Early Termination Makes Sense

**Good Reasons:**

- Equipment no longer needed (project completed)

- Better equipment available (tech upgrade)

- Consolidating fleet (downsizing)

- Cash flow crisis (reduce monthly obligations)

**Bad Reasons:**

- Minor inconvenience (penalty too high)

- Emotional decision (expensive mistake)

- Haven't checked damage fees first (surprise costs)

### Return at Lease End (No Penalty)

If you wait until the lease term expires, you can return the vehicle with **no early termination fee** - only damage penalties apply.

```

End-of-Lease Return Cost = Damage Penalties Only

Example:

Vehicle Damage: 15%

Damage Fee: $3,750 (15% × 25% × $100k)

Early Term Fee: $0 (lease completed)

───────────────────────────────

TOTAL COST: $3,750

```

---

## Damage Penalties

### Condition-Based Fees

When returning a leased vehicle, the lessor inspects for damage and charges penalties based on condition.

### Damage Fee Formula

```

Damage Fee = Vehicle Damage % × 25% × Original Price

Examples (on $100k tractor):

5% damage: $1,250 fee

10% damage: $2,500 fee

20% damage: $5,000 fee

50% damage: $12,500 fee

```

### What Counts as Damage?

**Chargeable Damage:**

- Body damage from collisions

- Paint wear and scratches

- Component damage (engine, hydraulic, electrical)

- Tire damage beyond normal wear

**Normal Wear (Not Charged):**

- Reasonable operating hours for lease term

- Standard tire tread wear within limits

- Minor cosmetic wear from field use

### Avoiding Damage Penalties

**Strategy 1: Maintain the vehicle**

- Keep damage below 10% during lease

- Repair damage before lease end

- Costs less than damage fee

**Strategy 2: Calculate repair vs. penalty**

```

Scenario: 20% damage on $100k tractor

Option A - Pay damage fee:

$5,000 (20% × 25% × $100k)

Option B - Repair before return:

$5,000 (20% × 25% repair cost)

Result: Usually same cost, but repairing adds value if you're buying out!

```

**Strategy 3: Buy instead of return**

If damage is high, buying out may be better than returning:

- Return: Pay damage fee + lose vehicle

- Buyout: Pay balloon + keep damaged vehicle (can repair later or sell as-is)

### Damage Inspection Report

When initiating a return, you receive a detailed inspection report:

```

LEASE RETURN INSPECTION

─────────────────────────────────────

Vehicle: John Deere 6R 150

Lease Term: 3 years (completed)

Operating Hours: 850 hours

CONDITION ASSESSMENT:

Body Damage: 18%

Paint Wear: 12%

Engine Health: 85%

Hydraulic Health: 78%

Electrical: 92%

DAMAGE FEES:

Body Damage: $4,500 (18% × 25% × $100k)

Paint Wear: $3,000 (12% × 25% × $100k)

Component Wear: $0 (acceptable condition)

─────────────────────────────────────

TOTAL DUE: $7,500

OPTIONS:

[Pay & Return] [Buyout Instead ($55k)]

```

---

## Credit Impact

### Leasing Affects Your Credit Score

Lease payments are treated the same as finance payments for credit scoring purposes.

### Credit Score Effects

| Action | Credit Impact | Notes |

|--------|---------------|-------|

| **On-Time Payment** | +2 points | Each monthly payment made on time |

| **Missed Payment** | -45 points | Severe penalty per missed month |

| **Early Buyout** | +15 points | Treated as "loan paid off early" |

| **Early Termination** | 0 points | Neutral (not a default) |

| **Lease Default** | -175 points | 3+ missed payments = seizure |

### Building Credit with Leases

Leasing is an excellent way to build credit:

**Advantages:**

- Lower payments = easier to pay on time

- Same credit boost as financing (+5/month)

- Early buyout gives big bonus (+50)

**Example Credit Journey:**

```

Starting Credit: 650 (Fair)

Lease Term: 3 years (36 months)

Payment History: 36 on-time payments

Credit Gain: +180 points (36 × +5)

Early Buyout Bonus: +15 points

─────────────────────────────────────

Ending Credit: 880 (Excellent)

```

### Credit Requirements for Leasing

Leasing has the **same credit requirements** as financing:

| Credit Score | Max Lease Term | Interest Adjustment |

|--------------|---------------|---------------------|

| 750+ (Excellent) | 5 years | -1.5% |

| 700-749 (Good) | 5 years | -0.5% |

| 650-699 (Fair) | 5 years | +0.5% |

| 600-649 (Poor) | 5 years | +1.5% |

| <600 (Very Poor) | 5 years | +3.0% |

**Note:** Unlike vehicle financing (which gates 11-15 year terms behind Good credit), leasing maxes at 5 years for everyone.

---

## Lease vs Finance

### When to Choose Leasing

**Lease if you:**

- Need lower monthly payments

- Plan to upgrade equipment regularly

- Aren't sure you'll keep it long-term

- Want to "try before you buy"

- Have seasonal or project-based needs

**Examples:**

- **Seasonal harvester** - Lease for harvest season, return afterward

- **Tech upgrade cycle** - Lease new model every 3 years

- **Cash flow management** - Lower payments free up capital

- **Testing equipment** - Use during lease, buy if you love it

### When to Choose Financing

**Finance if you:**

- Want to own the vehicle outright

- Plan to use it for 10+ years

- Need to sell or trade it later

- Want simplest total cost

- Don't want balloon payment surprise

**Examples:**

- **Workhorse tractor** - Keep forever, finance over 10-15 years

- **Fleet expansion** - Own assets, build equity

- **Resale value matters** - Own to sell when needed

### Side-by-Side Comparison

**Scenario:** $100,000 Tractor, 10% down, 5% interest, 3-year term

#### Financing

```

Down Payment: $10,000

Monthly Payment: $2,699

Total Payments: $97,164 (36 months)

Balloon Payment: $0

Final Ownership: Immediate (after down payment)

Can Sell: Yes, anytime

─────────────────────────────────────

TOTAL COST: $107,164

YOU OWN IT: After 3 years

```

#### Leasing

```

Down Payment: $10,000

Monthly Payment: $1,051

Total Payments: $37,836 (36 months)

Balloon Payment: $55,000 (to buy)

Final Ownership: After balloon paid

Can Sell: No (until buyout)

─────────────────────────────────────

TOTAL COST: $102,836 (if buyout)

YOU OWN IT: After 3 years + $55k

```

**Summary:**

- Lease saves $61/month in payments (61% lower!)

- Lease saves $4,328 total if you buy at the end

- But: Can't sell until buyout, must pay balloon

### Decision Framework

```

┌─────────────────────────────────────┐

│ Do you KNOW you'll keep it 5+ years?│

└──────────┬──────────────────────────┘

│

YES ───┴─── NO

│ │

│ │

┌────▼─────┐ ┌▼─────────────┐

│ FINANCE │ │ Balloon OK? │

│ │ └┬─────────────┘

│ - Own it │ │

│ - Equity │ YES ─── NO

│ - Resale │ │ │

└──────────┘ │ ┌───▼─────┐

┌───▼───┤ FINANCE │

│ LEASE ├─────────┘

│ │

│ - Low │

│ pay │

│ - Try │

└───────┘

```

---

## Tips & Strategies

### 1. Equipment Rotation Strategy

**The Strategy:** Lease equipment, use during lease term, return before it depreciates significantly.

**How it works:**

```

Year 1-3: Lease new $100k tractor ($1,051/month)

Year 3: Return tractor (minimal damage fees)

Year 3-6: Lease next-gen model (newer tech)

Year 6: Repeat cycle

Benefits:

- Always have latest equipment

- No long-term depreciation risk

- Predictable monthly costs

- Tax advantages (lease payments often deductible)

```

**Best for:** Large farms with regular equipment turnover needs

---

### 2. Lease-to-Own with Inspection

**The Strategy:** Lease used equipment, inspect hidden DNA quality during lease, buy only if it's a workhorse.

**How it works:**

```

1. Lease used equipment at lower price

2. During lease: Monitor reliability, check DNA hints

3. If workhorse DNA: Buy at lease end (keep forever)

4. If lemon DNA: Return at lease end (dodge bullet)

Example:

- Lease used $50k tractor (3-year term, $27.5k balloon)

- Use for 1 year, discover it's a lemon (constant repairs)

- Terminate lease early ($500 fee + $1,200 damage)

- Total loss: $13,300 (payments + fees)

- Avoided: $50k+ in long-term lemon ownership!

```

**Best for:** Risk-averse buyers who want to test before committing

---

### 3. Balloon Payment Savings Plan

**The Strategy:** Make balloon payment your "savings goal" during the lease term.

**How it works:**

```

Lease: $100k tractor, 5-year term

Monthly Payment: $1,046

Balloon Payment: $35,000

Savings Plan:

Set aside $585/month in savings (balloon ÷ 60 months)

At lease end: Use saved $35,100 to buy outright

Total monthly cost: $1,631 ($1,046 lease + $585 savings)

Compare to financing:

Finance payment: $1,887/month (5-year term)

Savings: $256/month vs financing

```

**Benefits:**

- Lower monthly obligation (flexibility)

- Build savings discipline

- Option to walk away if circumstances change

**Best for:** Disciplined savers who want flexibility

---

### 4. Short-Term Project Leasing

**The Strategy:** Lease specialized equipment for specific projects, return when done.

**How it works:**

```

Project: Clearing 50 acres of forest

Equipment Needed: $150k forestry mulcher

Project Duration: 6 months

Option A - Buy:

Purchase: $150,000

Use: 6 months (500 hours)

Resell: ~$120,000 (20% depreciation)

Net Cost: $30,000 + hassle

Option B - Lease (1-year term):

Down: $15,000 (10%)

Monthly: ~$3,800 × 6 = $22,800

Early Term: $2,280 (10% fee on remaining 6 months)

Damage Fee: $1,500 (minimal wear)

Net Cost: $41,580

Option C - Lease (2-year term):

Down: $15,000

Monthly: ~$2,100 × 6 = $12,600

Early Term: $1,890 (10% fee)

Damage Fee: $1,500

Net Cost: $30,990 (close to buying!)

Verdict: 2-year lease is best - similar cost to buying/selling but no resale hassle

```

**Best for:** One-time projects, specialized equipment

---

### 5. Credit Building Through Leasing

**The Strategy:** Use leases to rapidly build credit score through consistent payments.

**How it works:**

```

Starting Credit: 580 (Very Poor)

Strategy: Lease 3 smaller items with short terms

Lease 1: $20k trailer, 1-year term

Monthly: $600

Credit gain: +60 points (12 payments)

Lease 2: $30k implement, 2-year term

Monthly: $800

Credit gain: +120 points (24 payments)

Lease 3: $50k tractor, 3-year term

Monthly: $1,200

Credit gain: +180 points (36 payments)

After 3 years:

Total Credit Gain: +360 points

New Credit Score: 940 (capped at 850)

Actual Score: 850 (Excellent)

Benefits:

- Unlocked 15-year financing terms

- -1.5% interest rate discount

- Access to premium equipment

```

**Best for:** New farms building credit from scratch

---

### 6. The "Option Premium" Mindset

**The Strategy:** View the lease payment as paying for the OPTION to buy, not a commitment.

**How it works:**

```

Traditional Mindset:

"I'm paying $1,051/month toward owning this tractor"

Option Premium Mindset:

"I'm paying $1,051/month for:

- Use of this equipment NOW

- Right to buy for $55k later

- Ability to walk away if better tech emerges

- Flexibility if farm needs change"

Real Scenario:

Year 1-2: Use leased tractor

Year 2: New model released (20% more efficient)

Decision: Return leased tractor, lease new model

Result: Always have best equipment, minimal sunk cost

```

**Best for:** Tech enthusiasts, efficiency optimizers

---

### 7. Damage Management

**The Strategy:** Repair strategically before lease end to minimize penalties.

**When to repair:**

```

Damage Level: 15% ($3,750 penalty on $100k tractor)

Repair Cost: 15% × 25% × $100k = $3,750

Decision Matrix:

IF returning:

Repair cost ≈ Penalty → Doesn't matter (choose cheaper)

IF buying out:

ALWAYS repair before buyout

Reason: Repair adds value you'll own

Example:

Buyout price: $55,000

Damage: 20% ($5,000 penalty)

Option A - Buyout as-is:

Pay: $55,000

Own: Damaged tractor (worth $50k)

Net: -$5,000 (overpaid)

Option B - Repair then buyout:

Repair: $5,000

Buyout: $55,000

Own: Good tractor (worth $55k)

Net: $0 (fair deal)

```

**Best for:** Anyone planning to buy at lease end

---

### 8. The "Cash Flow Smoothing" Strategy

**The Strategy:** Use leasing to match equipment costs to revenue cycles.

**How it works:**

```

Farming Revenue Pattern:

Planting (Spring): Heavy expenses, no revenue

Growing (Summer): Low expenses, no revenue

Harvest (Fall): High expenses, HIGH revenue

Off-Season (Winter): Minimal activity

Traditional Purchase Problem:

Tractor purchase: $100k upfront (spring)

Cash flow: NEGATIVE $100k when you can least afford it

Leasing Solution:

Down payment: $10k (spring)

Monthly: $1,051 spread over 12 months

Cash flow: NEGATIVE $10k spring, then manageable monthly

Revenue Match:

Harvest revenue: $200k (fall)

Use surplus to:

- Cover 6 months payments in advance

- Save for next year's down payment

- Build balloon payment fund

```

**Best for:** Farms with seasonal cash flow

---

### 9. The "Trial Run" Strategy

**The Strategy:** Lease before committing to a major brand/model decision.

**How it works:**

```

Scenario: Choosing between Brand A and Brand B for $120k tractor

Option 1 - Buy Brand A:

Risk: $120k commitment

Problem: Might prefer Brand B after using it

Option 2 - Lease Brand A (1 year):

Cost: ~$3,500/month × 12 = $42,000

After 1 year:

- LOVE IT? → Buy out for $78k (total $120k)

- HATE IT? → Return, lease Brand B instead

Trial cost: $42k to avoid $120k mistake

```

**Best for:** First-time buyers, brand switchers

---

### 10. Advanced: The Arbitrage Play

**The Strategy:** Lease equipment, generate revenue, use profits to buy better equipment.

**How it works:**

```

Year 1:

Lease: $50k used baler (low payment)

Revenue: Custom baling for neighbors

Profit: $15k/year

Year 2:

Continue lease ($12k/year payments)

Profit: $15k

Net: +$3k

Year 3:

Accumulated profit: $9k

Lease end: $27.5k balloon

Decision: Return baler, use $9k + loan for NEW $80k baler

Result:

- Bootstrapped from $50k used to $80k new

- Minimal personal capital invested

- Revenue paid for upgrade

```

**Best for:** Custom work operators, contractors

---

## Summary

### Quick Reference Card

**When to Lease:**

- Lower monthly payments needed

- Short-term or seasonal use

- Testing equipment before buying

- Want flexibility to upgrade

**When to Finance:**

- Long-term ownership (5+ years)

- Need to own/sell the asset

- Avoid balloon payment complexity

- Simplest total cost structure

**Key Leasing Facts:**

- Monthly payments 40-60% lower than financing

- Cannot sell until buyout completed

- Damage penalties on return

- Same credit impact as financing

- Balloon payment required to own

**Critical Formula:**

```

Total Lease Cost = Down + (Monthly × Term) + Balloon + Damage Fees

Example:

= $10k + ($1,051 × 36) + $55k + $1,500

= $104,336 total cost to own via lease

```

---

**Last Updated:** 2026-02-18

**Version:** 2.15.0

For more information, see:

- [Vehicle Financing Guide](Vehicle-Financing.md)

- [Credit Scoring](Credit-Scoring.md)

- [Quick Start Guide](Quick-Start-Guide.md)

Lease Terms

UsedPlus offers flexible lease terms from 1 to 5 years.

### Available Terms

| Term | Monthly Payment | Residual Value | Total Interest | Best For |

|------|----------------|----------------|----------------|----------|

| **1 year** | Highest | 65% of price | Lowest | Short-term projects |

| **2 years** | High | 65% of price | Low | Seasonal use |

| **3 years** | Moderate | 55% of price | Moderate | Medium-term needs |

| **4 years** | Lower | 45% of price | Higher | Multi-year operations |

| **5 years** | Lowest | 35% of price | Highest | Long-term use |

### How Terms Affect Residual Value

The **residual value** (balloon payment) decreases with longer lease terms:

```

1-2 years: 65% of original price

3 years: 55% of original price

4 years: 45% of original price

5 years: 35% of original price

```

**Why it matters:** Longer leases mean lower balloon payments at the end, making buyout more affordable.

---

## Lower Monthly Payments

### Why Leasing Has Lower Payments

Leasing payments are lower than financing because **you're only paying for the depreciation during the lease period**, not the full vehicle value.

### Payment Comparison Example

**Scenario:** $100,000 Tractor, 10% down payment, 5% interest rate, 3-year term

#### Finance (Traditional Loan)

```

Principal: $90,000 (100k - 10k down)

Monthly Payment: $2,699

Total Payments: $97,164 (36 months)

Balloon Payment: $0

───────────────────────────────────

TOTAL COST: $107,164 (includes down payment)

YOU OWN IT: After 3 years

```

#### Lease

```

Principal: $90,000 (100k - 10k down)

Residual Value: $55,000 (55% of 100k for 3-year lease)

Effective Loan: $35,000 (90k - 55k)

Monthly Payment: $1,051

Total Payments: $37,836 (36 months)

Balloon Payment: $55,000 (to buy at end)

───────────────────────────────────

TOTAL IF BUYOUT: $102,836 (down + payments + balloon)

YOU OWN IT: After 3 years + balloon payment

```

**Result:**

- Lease monthly payment: $1,051 (61% lower!)

- BUT: Must pay $55k balloon to own it

- Financing total cost: $107,164

- Leasing total cost: $102,836 (saves $4,328 if you buy)

### The Catch

Lower monthly payments come with a tradeoff:

- You don't own the vehicle until you pay the balloon

- You can't sell a leased vehicle

- Early termination has penalties

- Damage at lease end incurs fees

---

## Residual Value (Balloon Payment)

### What is Residual Value?

The **residual value** is the estimated value of the vehicle at the end of the lease term. This is the amount you must pay to purchase (buy out) the leased vehicle.

### Residual Value by Term

| Lease Term | Residual % | Example ($100k Tractor) |

|------------|-----------|-------------------------|

| 1 year | 65% | $65,000 balloon |

| 2 years | 65% | $65,000 balloon |

| 3 years | 55% | $55,000 balloon |

| 4 years | 45% | $45,000 balloon |

| 5 years | 35% | $35,000 balloon |

### How Balloon Payments Work

At the end of your lease term, you have three options:

1. **Pay the balloon and own it** - Pay residual value in full

2. **Return the vehicle** - Walk away (minus damage fees)

3. **Extend/refinance** - Not currently available (future feature)

### Calculating Total Cost with Balloon

```

Total Lease Cost = Down Payment + (Monthly × Term) + Balloon Payment

Example (3-year, $100k tractor, 10% down):

= $10,000 + ($1,051 × 36) + $55,000

= $10,000 + $37,836 + $55,000

= $102,836

```

### Balloon Payment Strategies

**Strategy 1: Pay balloon immediately**

- Own the vehicle outright

- Total cost is down + payments + balloon

**Strategy 2: Finance the balloon**

- Take out a loan for the residual value

- Spreads balloon over additional years

- Converts lease into lease-to-own

**Strategy 3: Return the vehicle**

- Walk away at lease end

- Only paid down + monthly payments

- Good for equipment you only needed temporarily

---

## Buyout Option

### Purchase at Lease End

At the end of your lease term, you can **buy out** the vehicle by paying the residual value (balloon payment).

### Buyout Process

1. **Lease Term Ends**

- You receive notification that lease is complete

- Vehicle remains in your fleet (grace period)

2. **Decide: Buy or Return**

- **Buy:** Pay balloon payment in Finance Manager

- **Return:** Initiate return (damage fees assessed)

3. **After Buyout**

- Vehicle ownership transfers to you

- No more monthly payments

- Can now sell or trade the vehicle

- Full ownership benefits

### Early Buyout

You can buy out a leased vehicle **before** the lease term ends:

#### Early Buyout Formula

```

Early Buyout Cost = Remaining Lease Balance + Residual Value + Early Term Fee

Early Term Fee = 10% of remaining lease balance

```

#### Example: Early Buyout

**Scenario:** 5-year lease on $100k tractor, 2 years remaining

```

Remaining Lease Balance: $25,104 (24 months × $1,046)

Residual Value: $35,000

Early Termination Fee: $2,510 (10% of balance)

───────────────────────────────────────

TOTAL EARLY BUYOUT: $62,614

```

**Compare to:**

- Finishing lease + balloon: $60,104 (cheaper by $2,510)

- Early buyout penalty = 10% fee

**When to buy early:**

- You need to sell the vehicle urgently

- You want to trade it in toward a new purchase

- You found a great deal on a replacement and need cash

---

## Return Vehicle

### End Lease Early

You can return a leased vehicle before the term ends, but it comes with penalties.

### Early Termination Process

1. **Open Finance Manager** (press **Esc** → Finance Manager)

2. **Select Leased Vehicle**

3. **Click "Terminate Lease"**

4. **Damage Assessment**

- Inspector evaluates vehicle condition

- Damage penalties calculated

5. **Pay Termination Fees**

- Early termination fee (10% of remaining balance)

- Damage penalties (if applicable)

6. **Vehicle is Removed**

- Equipment disappears from your fleet

- Returned to lessor

### Early Termination Penalties

| Fee Type | Amount | Example (3-year, $100k tractor, 1 year left) |

|----------|--------|---------------------------------------------|

| **Early Term Fee** | 10% of remaining balance | $1,265 (10% × $12,648) |

| **Damage Fee** | Varies by condition | $0 - $15,000+ |

| **TOTAL PENALTY** | Both fees combined | $1,265 - $16,265+ |

### When Early Termination Makes Sense

**Good Reasons:**

- Equipment no longer needed (project completed)

- Better equipment available (tech upgrade)

- Consolidating fleet (downsizing)

- Cash flow crisis (reduce monthly obligations)

**Bad Reasons:**

- Minor inconvenience (penalty too high)

- Emotional decision (expensive mistake)

- Haven't checked damage fees first (surprise costs)

### Return at Lease End (No Penalty)

If you wait until the lease term expires, you can return the vehicle with **no early termination fee** - only damage penalties apply.

```

End-of-Lease Return Cost = Damage Penalties Only

Example:

Vehicle Damage: 15%

Damage Fee: $3,750 (15% × 25% × $100k)

Early Term Fee: $0 (lease completed)

───────────────────────────────

TOTAL COST: $3,750

```

---

## Damage Penalties

### Condition-Based Fees

When returning a leased vehicle, the lessor inspects for damage and charges penalties based on condition.

### Damage Fee Formula

```

Damage Fee = Vehicle Damage % × 25% × Original Price

Examples (on $100k tractor):

5% damage: $1,250 fee

10% damage: $2,500 fee

20% damage: $5,000 fee

50% damage: $12,500 fee

```

### What Counts as Damage?

**Chargeable Damage:**

- Body damage from collisions

- Paint wear and scratches

- Component damage (engine, hydraulic, electrical)

- Tire damage beyond normal wear

**Normal Wear (Not Charged):**

- Reasonable operating hours for lease term

- Standard tire tread wear within limits

- Minor cosmetic wear from field use

### Avoiding Damage Penalties

**Strategy 1: Maintain the vehicle**

- Keep damage below 10% during lease

- Repair damage before lease end

- Costs less than damage fee

**Strategy 2: Calculate repair vs. penalty**

```

Scenario: 20% damage on $100k tractor

Option A - Pay damage fee:

$5,000 (20% × 25% × $100k)

Option B - Repair before return:

$5,000 (20% × 25% repair cost)

Result: Usually same cost, but repairing adds value if you're buying out!

```

**Strategy 3: Buy instead of return**

If damage is high, buying out may be better than returning:

- Return: Pay damage fee + lose vehicle

- Buyout: Pay balloon + keep damaged vehicle (can repair later or sell as-is)

### Damage Inspection Report

When initiating a return, you receive a detailed inspection report:

```

LEASE RETURN INSPECTION

─────────────────────────────────────

Vehicle: John Deere 6R 150

Lease Term: 3 years (completed)

Operating Hours: 850 hours

CONDITION ASSESSMENT:

Body Damage: 18%

Paint Wear: 12%

Engine Health: 85%

Hydraulic Health: 78%

Electrical: 92%

DAMAGE FEES:

Body Damage: $4,500 (18% × 25% × $100k)

Paint Wear: $3,000 (12% × 25% × $100k)

Component Wear: $0 (acceptable condition)

─────────────────────────────────────

TOTAL DUE: $7,500

OPTIONS:

[Pay & Return] [Buyout Instead ($55k)]

```

---

## Credit Impact

### Leasing Affects Your Credit Score

Lease payments are treated the same as finance payments for credit scoring purposes.

### Credit Score Effects

| Action | Credit Impact | Notes |

|--------|---------------|-------|

| **On-Time Payment** | +2 points | Each monthly payment made on time |

| **Missed Payment** | -45 points | Severe penalty per missed month |

| **Early Buyout** | +15 points | Treated as "loan paid off early" |

| **Early Termination** | 0 points | Neutral (not a default) |

| **Lease Default** | -175 points | 3+ missed payments = seizure |

### Building Credit with Leases

Leasing is an excellent way to build credit:

**Advantages:**

- Lower payments = easier to pay on time

- Same credit boost as financing (+5/month)

- Early buyout gives big bonus (+50)

**Example Credit Journey:**

```

Starting Credit: 650 (Fair)

Lease Term: 3 years (36 months)

Payment History: 36 on-time payments

Credit Gain: +180 points (36 × +5)

Early Buyout Bonus: +15 points

─────────────────────────────────────

Ending Credit: 880 (Excellent)

```

### Credit Requirements for Leasing

Leasing has the **same credit requirements** as financing:

| Credit Score | Max Lease Term | Interest Adjustment |

|--------------|---------------|---------------------|

| 750+ (Excellent) | 5 years | -1.5% |

| 700-749 (Good) | 5 years | -0.5% |

| 650-699 (Fair) | 5 years | +0.5% |

| 600-649 (Poor) | 5 years | +1.5% |

| <600 (Very Poor) | 5 years | +3.0% |

**Note:** Unlike vehicle financing (which gates 11-15 year terms behind Good credit), leasing maxes at 5 years for everyone.

---

## Lease vs Finance

### When to Choose Leasing

**Lease if you:**

- Need lower monthly payments

- Plan to upgrade equipment regularly

- Aren't sure you'll keep it long-term

- Want to "try before you buy"

- Have seasonal or project-based needs

**Examples:**

- **Seasonal harvester** - Lease for harvest season, return afterward

- **Tech upgrade cycle** - Lease new model every 3 years

- **Cash flow management** - Lower payments free up capital

- **Testing equipment** - Use during lease, buy if you love it

### When to Choose Financing

**Finance if you:**

- Want to own the vehicle outright

- Plan to use it for 10+ years

- Need to sell or trade it later

- Want simplest total cost

- Don't want balloon payment surprise

**Examples:**

- **Workhorse tractor** - Keep forever, finance over 10-15 years

- **Fleet expansion** - Own assets, build equity

- **Resale value matters** - Own to sell when needed

### Side-by-Side Comparison

**Scenario:** $100,000 Tractor, 10% down, 5% interest, 3-year term

#### Financing

```

Down Payment: $10,000

Monthly Payment: $2,699

Total Payments: $97,164 (36 months)

Balloon Payment: $0

Final Ownership: Immediate (after down payment)

Can Sell: Yes, anytime

─────────────────────────────────────

TOTAL COST: $107,164

YOU OWN IT: After 3 years

```

#### Leasing

```

Down Payment: $10,000

Monthly Payment: $1,051

Total Payments: $37,836 (36 months)

Balloon Payment: $55,000 (to buy)

Final Ownership: After balloon paid

Can Sell: No (until buyout)

─────────────────────────────────────

TOTAL COST: $102,836 (if buyout)

YOU OWN IT: After 3 years + $55k

```

**Summary:**

- Lease saves $61/month in payments (61% lower!)

- Lease saves $4,328 total if you buy at the end

- But: Can't sell until buyout, must pay balloon

### Decision Framework

```

┌─────────────────────────────────────┐

│ Do you KNOW you'll keep it 5+ years?│

└──────────┬──────────────────────────┘

│

YES ───┴─── NO

│ │

│ │

┌────▼─────┐ ┌▼─────────────┐

│ FINANCE │ │ Balloon OK? │

│ │ └┬─────────────┘

│ - Own it │ │

│ - Equity │ YES ─── NO

│ - Resale │ │ │

└──────────┘ │ ┌───▼─────┐

┌───▼───┤ FINANCE │

│ LEASE ├─────────┘

│ │

│ - Low │

│ pay │

│ - Try │

└───────┘

```

---

## Tips & Strategies

### 1. Equipment Rotation Strategy

**The Strategy:** Lease equipment, use during lease term, return before it depreciates significantly.

**How it works:**

```

Year 1-3: Lease new $100k tractor ($1,051/month)

Year 3: Return tractor (minimal damage fees)

Year 3-6: Lease next-gen model (newer tech)

Year 6: Repeat cycle

Benefits:

- Always have latest equipment

- No long-term depreciation risk

- Predictable monthly costs

- Tax advantages (lease payments often deductible)

```

**Best for:** Large farms with regular equipment turnover needs

---

### 2. Lease-to-Own with Inspection

**The Strategy:** Lease used equipment, inspect hidden DNA quality during lease, buy only if it's a workhorse.

**How it works:**

```

1. Lease used equipment at lower price

2. During lease: Monitor reliability, check DNA hints

3. If workhorse DNA: Buy at lease end (keep forever)

4. If lemon DNA: Return at lease end (dodge bullet)

Example:

- Lease used $50k tractor (3-year term, $27.5k balloon)

- Use for 1 year, discover it's a lemon (constant repairs)

- Terminate lease early ($500 fee + $1,200 damage)

- Total loss: $13,300 (payments + fees)

- Avoided: $50k+ in long-term lemon ownership!

```

**Best for:** Risk-averse buyers who want to test before committing

---

### 3. Balloon Payment Savings Plan

**The Strategy:** Make balloon payment your "savings goal" during the lease term.

**How it works:**

```

Lease: $100k tractor, 5-year term

Monthly Payment: $1,046

Balloon Payment: $35,000

Savings Plan:

Set aside $585/month in savings (balloon ÷ 60 months)

At lease end: Use saved $35,100 to buy outright

Total monthly cost: $1,631 ($1,046 lease + $585 savings)

Compare to financing:

Finance payment: $1,887/month (5-year term)

Savings: $256/month vs financing

```

**Benefits:**

- Lower monthly obligation (flexibility)

- Build savings discipline

- Option to walk away if circumstances change

**Best for:** Disciplined savers who want flexibility

---

### 4. Short-Term Project Leasing

**The Strategy:** Lease specialized equipment for specific projects, return when done.

**How it works:**

```

Project: Clearing 50 acres of forest

Equipment Needed: $150k forestry mulcher

Project Duration: 6 months

Option A - Buy:

Purchase: $150,000

Use: 6 months (500 hours)

Resell: ~$120,000 (20% depreciation)

Net Cost: $30,000 + hassle

Option B - Lease (1-year term):

Down: $15,000 (10%)

Monthly: ~$3,800 × 6 = $22,800

Early Term: $2,280 (10% fee on remaining 6 months)

Damage Fee: $1,500 (minimal wear)

Net Cost: $41,580

Option C - Lease (2-year term):

Down: $15,000

Monthly: ~$2,100 × 6 = $12,600

Early Term: $1,890 (10% fee)

Damage Fee: $1,500

Net Cost: $30,990 (close to buying!)

Verdict: 2-year lease is best - similar cost to buying/selling but no resale hassle

```

**Best for:** One-time projects, specialized equipment

---

### 5. Credit Building Through Leasing

**The Strategy:** Use leases to rapidly build credit score through consistent payments.

**How it works:**

```

Starting Credit: 580 (Very Poor)

Strategy: Lease 3 smaller items with short terms

Lease 1: $20k trailer, 1-year term

Monthly: $600

Credit gain: +60 points (12 payments)

Lease 2: $30k implement, 2-year term

Monthly: $800

Credit gain: +120 points (24 payments)

Lease 3: $50k tractor, 3-year term

Monthly: $1,200

Credit gain: +180 points (36 payments)

After 3 years:

Total Credit Gain: +360 points

New Credit Score: 940 (capped at 850)

Actual Score: 850 (Excellent)

Benefits:

- Unlocked 15-year financing terms

- -1.5% interest rate discount

- Access to premium equipment

```

**Best for:** New farms building credit from scratch

---

### 6. The "Option Premium" Mindset

**The Strategy:** View the lease payment as paying for the OPTION to buy, not a commitment.

**How it works:**

```

Traditional Mindset:

"I'm paying $1,051/month toward owning this tractor"

Option Premium Mindset:

"I'm paying $1,051/month for:

- Use of this equipment NOW

- Right to buy for $55k later

- Ability to walk away if better tech emerges

- Flexibility if farm needs change"

Real Scenario:

Year 1-2: Use leased tractor

Year 2: New model released (20% more efficient)

Decision: Return leased tractor, lease new model

Result: Always have best equipment, minimal sunk cost

```

**Best for:** Tech enthusiasts, efficiency optimizers

---

### 7. Damage Management

**The Strategy:** Repair strategically before lease end to minimize penalties.

**When to repair:**

```

Damage Level: 15% ($3,750 penalty on $100k tractor)

Repair Cost: 15% × 25% × $100k = $3,750

Decision Matrix:

IF returning:

Repair cost ≈ Penalty → Doesn't matter (choose cheaper)

IF buying out:

ALWAYS repair before buyout

Reason: Repair adds value you'll own

Example:

Buyout price: $55,000

Damage: 20% ($5,000 penalty)

Option A - Buyout as-is:

Pay: $55,000

Own: Damaged tractor (worth $50k)

Net: -$5,000 (overpaid)

Option B - Repair then buyout:

Repair: $5,000

Buyout: $55,000

Own: Good tractor (worth $55k)

Net: $0 (fair deal)

```

**Best for:** Anyone planning to buy at lease end

---

### 8. The "Cash Flow Smoothing" Strategy

**The Strategy:** Use leasing to match equipment costs to revenue cycles.

**How it works:**

```

Farming Revenue Pattern:

Planting (Spring): Heavy expenses, no revenue

Growing (Summer): Low expenses, no revenue

Harvest (Fall): High expenses, HIGH revenue

Off-Season (Winter): Minimal activity

Traditional Purchase Problem:

Tractor purchase: $100k upfront (spring)

Cash flow: NEGATIVE $100k when you can least afford it

Leasing Solution:

Down payment: $10k (spring)

Monthly: $1,051 spread over 12 months

Cash flow: NEGATIVE $10k spring, then manageable monthly

Revenue Match:

Harvest revenue: $200k (fall)

Use surplus to:

- Cover 6 months payments in advance

- Save for next year's down payment

- Build balloon payment fund

```

**Best for:** Farms with seasonal cash flow

---

### 9. The "Trial Run" Strategy

**The Strategy:** Lease before committing to a major brand/model decision.

**How it works:**

```

Scenario: Choosing between Brand A and Brand B for $120k tractor

Option 1 - Buy Brand A:

Risk: $120k commitment

Problem: Might prefer Brand B after using it

Option 2 - Lease Brand A (1 year):

Cost: ~$3,500/month × 12 = $42,000

After 1 year:

- LOVE IT? → Buy out for $78k (total $120k)

- HATE IT? → Return, lease Brand B instead

Trial cost: $42k to avoid $120k mistake

```

**Best for:** First-time buyers, brand switchers

---

### 10. Advanced: The Arbitrage Play

**The Strategy:** Lease equipment, generate revenue, use profits to buy better equipment.

**How it works:**

```

Year 1:

Lease: $50k used baler (low payment)

Revenue: Custom baling for neighbors

Profit: $15k/year

Year 2:

Continue lease ($12k/year payments)

Profit: $15k

Net: +$3k

Year 3:

Accumulated profit: $9k

Lease end: $27.5k balloon

Decision: Return baler, use $9k + loan for NEW $80k baler

Result:

- Bootstrapped from $50k used to $80k new

- Minimal personal capital invested

- Revenue paid for upgrade

```

**Best for:** Custom work operators, contractors

---

## Summary

### Quick Reference Card

**When to Lease:**

- Lower monthly payments needed

- Short-term or seasonal use

- Testing equipment before buying

- Want flexibility to upgrade

**When to Finance:**

- Long-term ownership (5+ years)

- Need to own/sell the asset

- Avoid balloon payment complexity

- Simplest total cost structure

**Key Leasing Facts:**

- Monthly payments 40-60% lower than financing

- Cannot sell until buyout completed

- Damage penalties on return

- Same credit impact as financing

- Balloon payment required to own

**Critical Formula:**

```

Total Lease Cost = Down + (Monthly × Term) + Balloon + Damage Fees

Example:

= $10k + ($1,051 × 36) + $55k + $1,500

= $104,336 total cost to own via lease

```

---

**Last Updated:** 2026-02-18

**Version:** 2.15.0

For more information, see:

- [Vehicle Financing Guide](Vehicle-Financing.md)

- [Credit Scoring](Credit-Scoring.md)

- [Quick Start Guide](Quick-Start-Guide.md)